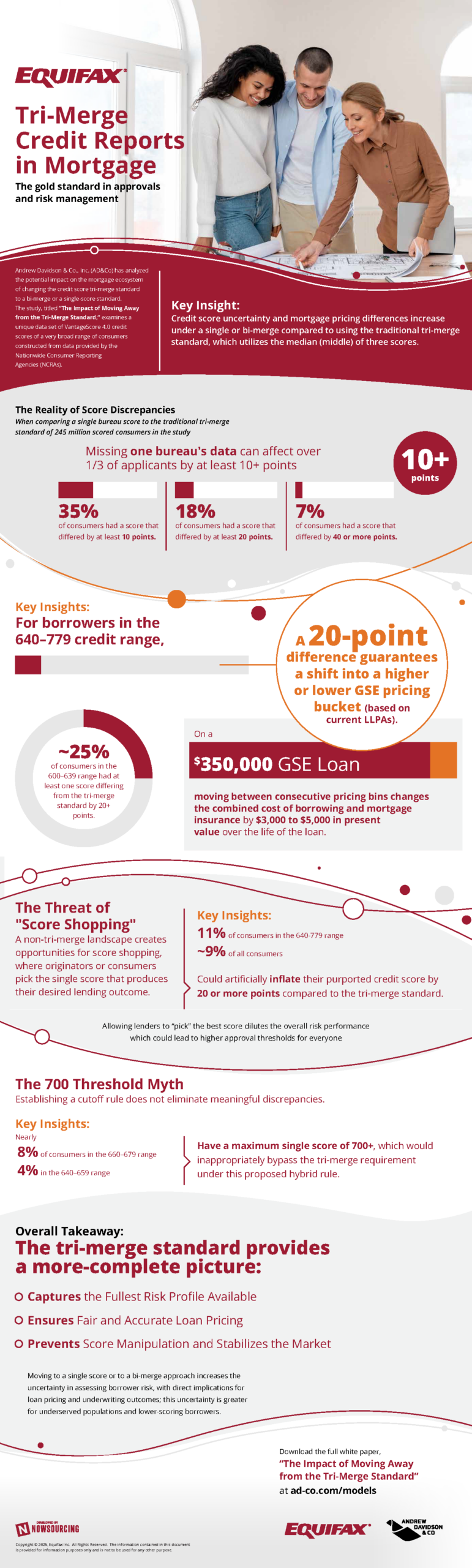

When it comes to pricing mortgages and other loans, an individual’s financial factors are a very large contributor. Credit information from reputable bureaus like Equifax, TransUnion, and Experian are pivotal to determining a prospective borrower’s price especially. For this reason, the standard for lenders has been to accumulate the scores from those 3 credit bureaus, which is known as a tri-merge credit report. However, recently some lenders have used bi-merge credit reports, which omits one of these 3 credit bureaus. So how much can omitting 1 bureau really do?

It is estimated that by only ordering reports from 2 credit bureaus, as much as 35% of prospective borrowers can see a credit score 10 or more points away from their tri-merge credit score. Furthermore, around 1 in every 5 consumers see a discrepancy of 20 or more points. While such a score differential can seem small, it has a big impact on pricing. In fact, a 20-point difference ensures that a consumer is placed in the incorrect pricing bucket for their loan. On a $350,000 loan, that equates to a dollar difference anywhere between $3,000 and $5,000.

Using a bi-merge credit report also allows consumers to game the system. When lenders use all 3 bureaus, these lenders all arrive at the same credit score. However, when only 2 of the 3 are used, the credit score a lender arrives at depends on which 2 bureaus were used. This allows consumers to shop around until they find a credit score that is best for them. This could not only lead to lenders taking on more risk, but they are also leaving money on the table.

Ultimately, accuracy about financial status is paramount when it comes to pricing a loan. To avoid situations with mispriced loans and customers gaming the system, ordering reports from all 3 bureaus is essential.